VC Value-Add Is a Myth? Only When Executed Poorly.

And it's both VCs and founders to blame.

Criticism of the “VC Platform” profession (i.e., the role in VC primarily responsible for the value creation component) is a boomerang in industry conversations, always coming back around.

Twitter, LinkedIn, and Instagram are full of memes about VCs “adding value” (like the one below).

Last year, Kate Clark’s article “Why VC's Platform Teams Are on the Chopping Block” generated considerable buzz among the platform professionals' community who disagreed with the statement that “…firms should run their shops like pro sports teams. Get rid of the poor performers [portfolio services team members] and optimise the roster.”

The recent summary of Fortune’s 2024 Brainstorm Tech conference in Park City, Utah, “What GPs and LPs say to each other behind closed doors” by Allie Garfinkle, features a spicy comment of one of the attendees saying that “VC platforms are BS” and claiming that VCs using platforms to court founders are just posturing. Platforms meant to offer resources beyond funding are seen as unnecessary distractions by founders. They prefer direct access to partners over constant platform support. This comment, again, caused a lot of disagreement among the audience.

Contrasting Views on VC’s Role

It seems to be a controversial topic in the entrepreneurial community that is divided into two groups:

(1) Self-Reliance Advocates: People who believe that VC exists to write checks and pick exceptional founders who don’t need any support because the GPs wouldn’t back them in the first place

(2) Collaborative Partners: People who believe VC funds should offer smart money. Once they invest, they become almost an extension of the founding team and do everything they can to contribute to the company's success.

So, in an attempt to do a reality check, it’s worth considering facts, not opinions, to answer the controversial question: Is VC platform BS?

Fact 1: Founders want their investors to help

The Forward More Than Money Report 2021 indicates that 61% of founders want more than money. The number is even higher if we look at female founders (a vastly underrepresented group in most ecosystems worldwide): 86% of female founders consider value-add necessary when picking a VC - that's 26% more than their male counterparts.

Another report, The Frontline What Founders Want, shows that founders see VCs as an extension of their sales team: 63% of US-based founders (30% in Europe) chose ‘introductions to prospective customers’ as one of the three factors they consider when selecting VCs. Other ‘value add’ factors considered include fundraising support, help to expand into new markets, help to hire talent, peer network and PR support (these, in fact, are the primary platform categories defined: see VC Platform Strategy Matrix by Cory Bolotsky).

The research Do VCs add value?, led by three Kauffman Fellows, confirms that founders believe VCs can help in three main areas: fundraising (39%), founder coaching (17%), and hiring support (14%).

Founders can exist without Venture Capital, but VCs are helpless without founders. The power dynamic is clear: VCs must bend or break.

Though only a tiny fraction of companies raise venture capital, many of the biggest tech successes—Google, LinkedIn, Twitter, Facebook, Apple, Cisco, Uber —did. Half of all US public companies founded since 1970 had VC support. This underscores the critical role venture capital plays in shaping the future of innovation and the global economy, acting as the driving force behind many of the most transformative companies in history.1

Fact 2: Funds with value creation platforms perform better

These VC funds that listen to founders and provide value-added services have historically outperformed those that don’t.

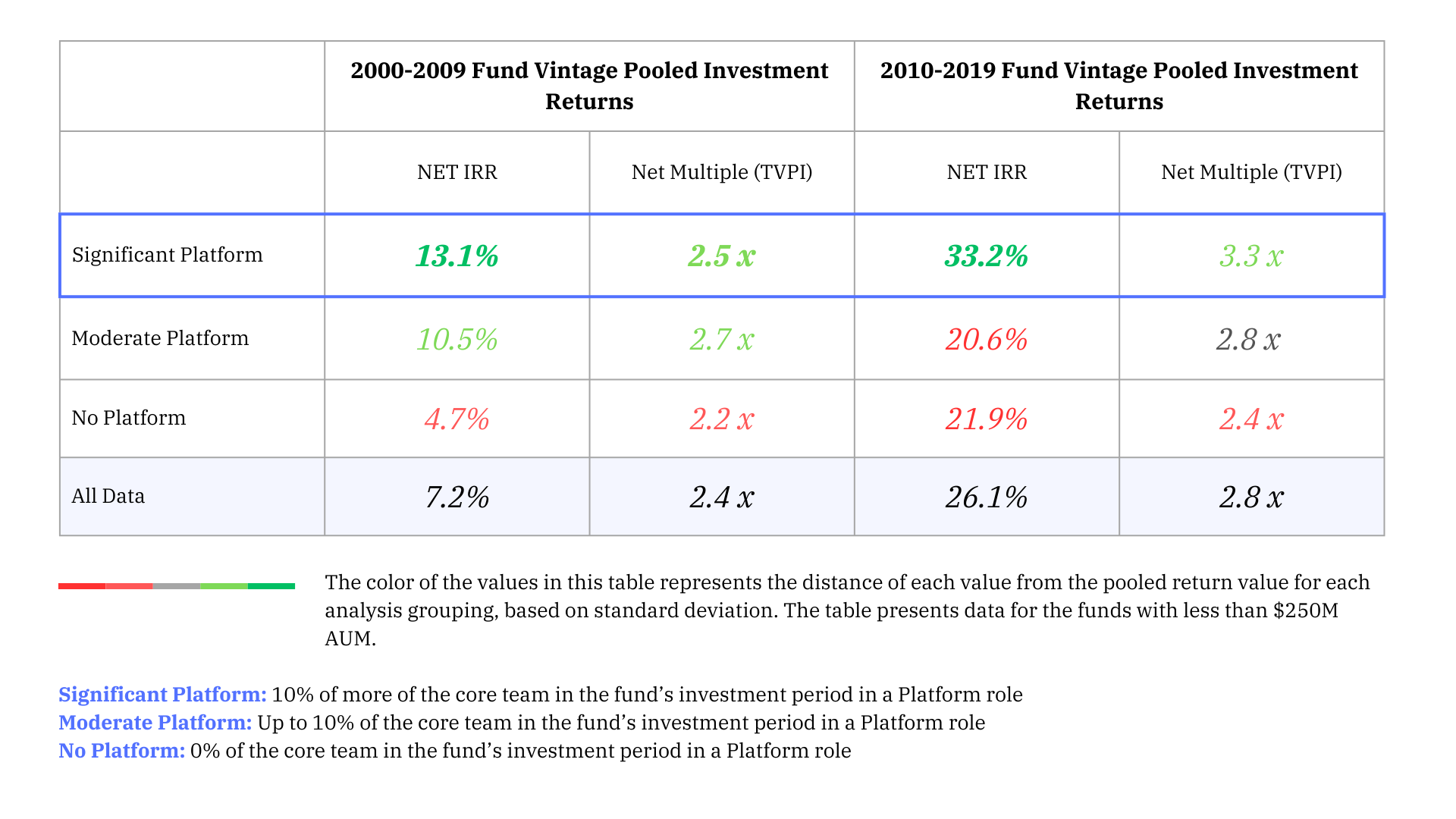

The VC Platform Community analysed 850 VC firms between 2020-2022 and found that VCs with Significant Platform produced 1,160 basis point improvements in Net IRR and 0.9x TVPI compared to VCs with No Platform in the last decade.

As the Platform function has matured over the last 10 years, the difference in fund performance across these categorical cohorts is far more pronounced than in the early years of the century.

Reality check: Founders often don’t know how to ask for help

As a venture capitalist, I frequently encounter founders who express frustration over not receiving the promised benefits from their so-called "value-add" investors. However, are the founders fully aware of how to leverage the potential value their investors could offer?

Sam Corcos, the founder of Levels, shared an interesting point of view in my all-time favourite Lenny’s Newsletter post:

”Between June 27, 2019, and October 26, 2022 (about 3 years and 4 months), I facilitated 2,626 requests through our investor network. Out of those, 1,664 received a response, and 1,151 successfully delivered on the ask.”

The reality is that investors typically have limited insight into the day-to-day workings of your company or your immediate needs. Expecting them to proactively offer value without clear guidance is unrealistic. Founders need to develop the skill of making precise, actionable requests—a task that may seem straightforward but actually requires significant practice, and many founders struggle with it.”

Levels’ cap table includes A16Z, Long Journey Ventures, TriplePoint Capital and many prominent angel investors, including Lenny Rachitsky. 60% of them tried to help, and every 7 out of 10 responses to the founders’ request met his expectations. Not bad, right?

Reality check: VCs often overpromise and underdeliver

VCs like to think they’re adding value, but founders don't always agree. In 2021, 92% of VCs said they were value-add investors, yet 61% of founders rated their experience below average (Full report). The numbers back it up: in 2018, VCs rated their impact on portfolio companies as a 7 out of 10. Founders gave them a 5.3. By 2022, nothing had changed—VCs still rated themselves a 7, while founders scored them even lower, at 5.2 (Full article). The gap is clear, but it’s not surprising. VCs think they're helping, but founders are looking for something they’re not getting.

To add to this, founders often say that VCs' value-added efforts aren’t goal-oriented. What’s the problem, then? No one knows what the end result is supposed to be. If there’s no clear target, it’s hard to measure success—or even see if you’re on the right track. VCs might think they’re helping, but without a clear goal, it’s just noise.

Proactive VCs with a clear superpower win

A proactive portfolio strategy outperforms a reactive one by intentionally creating value rather than waiting for founders to request support. It actively drives value instead of waiting for founders to seek assistance. With a clear plan in place, VCs are not just responding to problems—they're preventing them and aligning efforts with financial outcomes. By leveraging pattern recognition, VCs can anticipate potential challenges and take action before they become issues.

As my fellow platform leader, Dan Kozikowski of FirstMark, put it: “The question isn’t whether the Platform works. It’s whether your Platform is working toward the right things.” The key is focusing on one superpower that can become the fund differentiator. For example, YCombinator would probably put fundraising as their superpower, and 500 Global might cite their global network (at Seedstars International, the focus is on growth).2

In the end, success comes from proactiveness and a clear focus. By adding value early and honing a specific strength, VCs can stand out and deliver real results.

Final thoughts

As the startup ecosystem evolves, the relationship between founders and VCs is bound to become even more collaborative. Founders and VCs clearly need more upfront discussions to align expectations from the start. Founders should also put effort into thoroughly vetting their investors to ensure the best fit. Doing due diligence on VCs is just as crucial for founders as it is for investors.

VC Investors adding value are BS only when executed poorly… by both.

Strebulaev, I., & Dang, A. (2024). The venture mindset: How to make smarter bets and achieve extraordinary growth.